The Georgian wine market was dramatically damaged by the Russian wine embargo. The government response to this has been to aggressively promote Georgian wines abroad. Prior to the war there were some indications that this strategy was at least helping in the exports of relatively high-priced wines. It has, however, created two vulnerabilities. First, the higher end wine market has been hit hard by the global recession and so Georgian wine exports for 2009 are significantly lower than 2008. Second, high-end niche marketing seems unlikely to create the dramatic volume increases in sales that would be necessary to help small Georgian wine producers.

Following the Georgian wine ban in March 2006, exports dropped to around 15% its pre-ban level in volume terms.

Reference: Department of Statistics Food Security Situation (Issue 39 p13 and issue 40 p14)

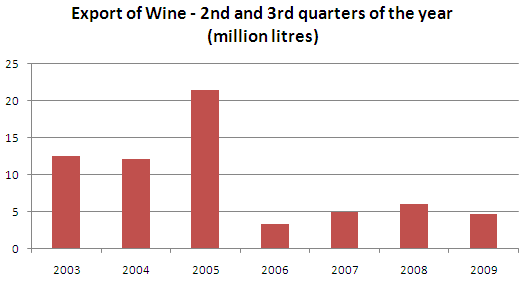

In order to allow meaningful comparison this graph compares wine export during the 2nd and 3rd quarters of 2003-2009 (first quarter is excluded because in 2006 it predates the wine-ban and fourth quarter is excluded because it is not available for 2009).

Obviously, these figures only relate to six months sales so are about half the total volume for any particular year. However, they show that while there was some recovery in 2007 and 2008, in 2009 the volume has dropped back sharply. The most obvious explanation for this is the global recession. However, the wine market seems buoyant globally so this does not provide the simple explanation that one might think.

Part of the reason why Georgian wine has been hit by the recession is almost certainly price. The average liter of wine sold before the Russian wine ban was exported at $1.95 per liter ($1.46 per bottle). The average liter sold in 2006 after the wine ban exported at $3.61 per liter ($2.70 per bottle). The overall price has dropped a little since that time, but not much, with average price for exporting ranging between $3.10-$3.40 per liter in 2007-2009 (deduced from same source as the chart above).

This is the equivalent of $2.30 to $2.50 per bottle and translates into a retail price in Europe or the US of $10 per bottle or more and puts Georgian wine as a relatively highly priced developing world wine. This probably explains why the recession has hurt Georgian exports of wine since while wine exports have gone up globally, more expensive wine sales have gone down.

It also shows, perhaps unsurprisingly, that any recovery taking place in the wine business has been driven by big producers who are able to produce wine to be marketed to the west for high prices. For them the wine ban may have been something of a blessing since it has allowed them to focus on the far more profitable end of their market.

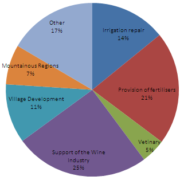

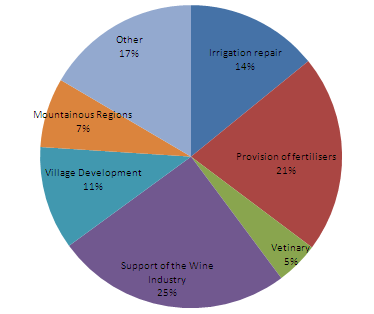

However, it suggests little or no recovery for the majority of small wine producers. This is a massive problem for the country and has created a number of immediate effects. First, according to the World Bank Poverty report Kakheti is now the second poorest region in Georgia with a poverty head-count of 46% (though as I suggested before, this does not include the poorest region of Racha-Lechkhumi and Kvemo-Svaneti – see previous blog). Second, support for the wine industry now takes up 25% of the budget of the Ministry of Agriculture, or GEL 28.5 million (USD 17.2 million).

Reference:Ministry of Finance: Programmatic Budget for 2009

As a proportion of the government’s overall spending the support for wine is very small (less than 0.5%). The problem is that it encourages farmers to remain in an industry that is has little prospect of growth in the short-to-medium term.

Demand for wine produced by small producers seems unlikely to grow significantly in the short-term for two main reasons. First, the local market is almost certainly saturated. Certainly, unlike other areas of agribusiness, there is little choice for import substitution (since Georgians do not drink imported wine). For the local population to absorb the spare capacity every adult in Georgia would have to drink around 15 extra bottles of wine per year. Or perhaps more realistically, every adult MALE would have to drink 33 bottles of wine. Second, there are no other local markets that seem likely as Russia substitutes for the cheaper/poorer quality wine.

It seems that the one hope for small local producers is that the large producers will grow fast enough to dramatically increase the demand for grapes. On this there may be some grounds for optimism but overall the situation remains difficult. Exports did increase by 80% in the two years following the wine ban even that still left them at less than a third of pre-ban levels. However, it seems unrealistic to expect this growth curve to continue since it only occurred after a dramatic push by the government, wine producers and international organizations and because the high-end niche that the Georgians producers have so far targeted, is by its very nature, fairly small.

All of this is not to suggest that the government should give up a push for wine exports or abandon agricultural support for grape/wine makers. However, what it does seem to suggest is that for the country as a whole encouraging people to move out of grape production and into more lucrative agribusiness may be a useful supplement to the existing strategy and certainly more effective than simply buying unwanted grapes indefinitely.