By George Welton, Executive Director, GeoWel Research and

Stephanie Komsa, Komsa International

The Poti Free Industrial Zone (FIZ) is promoted to offer broad tax benefits to companies who establish operations in the zone. Companies operating in the FIZ are not subject to corporate taxes, property taxes, and customs taxes on imported inputs, and they are also exempt from VAT charges. In order to better understand the costs and benefits of operating in the Poti FIZ, we calculated the overall impact on profitability of opening a medium-sized light manufacturing factory, fictitiously called Rustaveli Inc., inside the zone as opposed to outside the zone.

Overall, we found that the tax savings significantly outweigh the additional costs of opening a business and operating in the FIZ. In our imaginary company, with turnover of $3 million and capital investments of $2 million in the first year, the overall tax versus cost saving was $53,093, or an 18% increase in profits, along with a significant cash-flow saving from VAT.

Overall Cost-Benefit Analysis

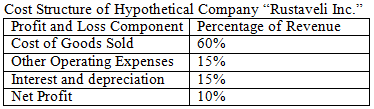

In our imagined case, Rustaveli Inc has an annual turnover of $3 million, imports 50% of its inputs, exports 50% of its finished products, and has the cost structure shown in the table below. We also assume that the company invests $2 million to build its facility and purchase equipment. Purchase of land is not included as land can only be rented in the Rakia FIZ.

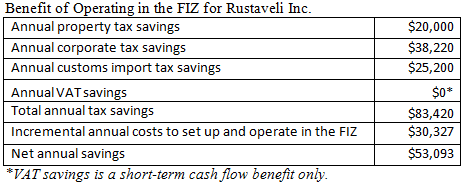

In our fictitious example Rustaveli Inc. incurs a $30,327 annual cost as a result of operating in the FIZ which it would not incur if it operated outside. However, it gains $83,420 in annual tax savings, as shown in the table below. This results in a net savings of $53,093, or approximately 18% of Rustaveli Inc.’s annual net profit. Rustaveli Inc. also benefits from a significant short-term cash flow savings as a result of being exempt from paying VAT on inputs. The savings estimated here along with the VAT cash flow benefit can be expected to grow along with overall growth of the imagined company.

To come to our conclusion, we first considered the incremental costs to operate in the FIZ. Based on information provided by Rakia, we calculated $16,800 in charges for setting up a business in the Rakia free zone. This includes $3,300 in registration costs and an estimated $3,500 in various other fixed costs and fees. We also assume that opening in the FIZ would require legal costs over and above those associated with starting a normal company and we have estimated this cost at $10,000. We do not include the costs of building permits and utility connections in the FIZ since these are similarly priced to what they would cost outside. Assuming the $16,800 incremental start up cost is financed locally at 18% and paid back over 5 years, it represents an annual charge of $5,119.

In addition, there are a number of annual costs associated with operating in the FIZ. There is an $8,000 annual license, charges for employee and vehicle registration and for visiting employees and vehicles, as well as some other annual charges. We also include an estimate of approximately $4,500 for the additional on-going legal and administrative costs that would likely be associated with operating in the FIZ. When we combine these annual costs with the amortized start-up charges, the total additional annual cost to operate in the FIZ for Rustaveli Inc. is $30,327.

These costs do not take into account differences in land-rental prices inside and outside the zone. As land in the FIZ cannot be purchased, any company operating in the FIZ would have to rent space. Land rental prices in the Poti FIZ vary according to usage, but Rakia told us that our imagined company would be charged $6 per square meter for land (which can be built on) plus $30 per square meter for any factory shell or warehousing provided by Rakia. They would also charge for any land cleaning or leveling required. We did not compare this cost to the cost of purchasing, renting and/or constructing facilities in Georgia outside of the FIZ because the variation is too great to make comparison meaningful. We do conclude, however, that rental costs in the FIZ would likely be somewhat more expensive than market prices in Georgia outside of the FIZ.

Against these costs, there are four main benefits of operating in the FIZ: corporate profit tax savings, property tax savings, customs tax savings and a short-term VAT cash flow benefit.

Tax Savings

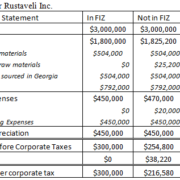

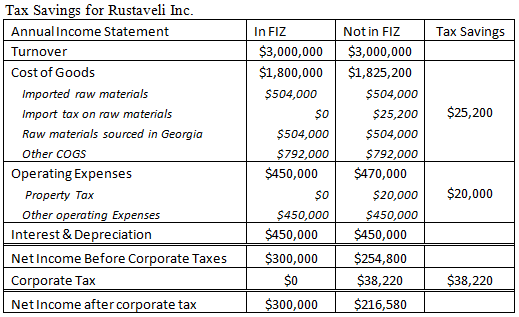

The most obvious tax saving is corporate tax, which is not charged in the zone. Profit tax is 15% in Georgia and so the saving in our case is $38,220.

The second tax saving is on property tax. Land can be rented in the FIZ only, not purchased; thus, this benefit applies only to property tax on the company’s plant and equipment. The property tax on these items is 1% and so in our case is a $20,000 annual savings on a $2 million investment.

The third tax saving is on customs import tax. Imported inputs are not subject to import tax in the FIZ, but a number of goods are subject to an import tax in the rest of Georgia. Changes to the tax code this year have increased the range of products that are subject to an import tax, which can range up to 12%.The exact burden will depend upon the type of products imported. For our case we assume that if Rustaveli Inc. were operating in Georgia outside of the FIZ, it would incur an average import tax on inputs of 5% (this average assumes that some inputs would be taxed while others would not). As we assume half of its raw material inputs are imported, this tax savings is equal to $25,200.

The corporate tax, property tax and import tax benefits can be seen in the annual income statement for Rustaveli Inc. presented below:

VAT Cash Flow Benefit

The final potential tax benefit is related to VAT. Inputs moving into the zone either from abroad or from the rest of Georgia are not subject to VAT, and so companies operating in the FIZ will not have to pay VAT on their inputs. However, since a company operating outside the zone would be able to reclaim this VAT payment anyway, this will improve the timing of cash-flow only rather than bottom-line profitability.

Although this is only a short-term cash-flow benefit, it could be particularly valuable during the start-up phase, when companies in Georgia typically pay out a large amount of VAT for capital expenditures. In our case the VAT that would be paid during the start-up period, if operating outside the zone, could be over $250,000 (18% of an estimated 70% of the $2,000,000 plant and equipment investment).

The VAT cash-flow benefit can also be useful for exporters, because large exporters typically have to wait for VAT reimbursements from the government since they do not have domestic sales on which they collect VAT. In our case, the value of the short-term operating cash-flow benefit is $223,740 annually.

Rules of Origin and their Consequences

While inputs are not subject to import tax in the zone, how the finished goods are taxed when they leave the FIZ to be sold in Georgia will depend on whether they are deemed ‘made in Georgia’. The ‘made in Georgia’ classification is vital because if goods are not deemed to be “made in Georgia,” then when a company operating in the FIZ sells its goods to customers in Georgia proper, its customers must pay import taxes as if the products were being imported from outside of the country. This would not be a direct cost to the company operating in the FIZ, but would affect its price competitiveness, as its customers in Georgia would have to pay the tax. However, this would apply only if the goods are deemed not to be “made in Georgia” and if the types of goods being sold are subject to an import tax in Georgia.

While Rakia is confident that all goods produced in the zone will be classified ‘made in Georgia’, the guidelines that govern this classification are somewhat complicated and seem to present some contradictions. For a start, article 10 of the rules governing the classification states that “easy construction operations” will not be considered as the basis for determining origin. Also, one criterion of the rules of origin says that goods are considered to have originated from a certain country if more than 51% of its inputs are from that country. Another criteria says that they originate in the last place they are produced. The rules do not say what is done if these criteria contradict.

In the case of Rustaveli Inc, if its products were subject to the Georgian import tax, this would be an extra $75-180,000 annual cost (assuming 5% to 12% import tax rate) to its Georgian customers.

The “made in Georgia” issue is also important for goods that are sold into countries with which Georgia holds trade agreements. Products leaving the FIZ that are deemed “made in Georgia” can enjoy the same free-trade access that Georgia enjoys with many CIS countries and Turkey, as well as access to Europe and America under the GSP+ provisions. If goods are not deemed “made in Georgia”, they will not gain these benefits.

Any producer would need to gain clarification on this issue prior to making an investment decision if it was selling a significant amount of its products into Georgia or to countries that have bilateral or regional trade agreements with Georgia. For Rustaveli Inc, we have assumed that its products are considered “made in Georgia” and so not subject to the import tax when selling into Georgia.

Overall, the tax case for producing in the FIZ seems clearly positive. Ideally the rules of origin need to be clarified to give investors added confidence regarding sales in Georgia and the region. However, in our analysis the overall savings can be significant, particularly for companies that import large quantities of their inputs (due to the customs tax savings), and for export-oriented companies as result of the potential VAT cash flow benefit. Investors and businesses that consider establishing themselves in the FIZ must of course conduct their own analysis, but our case demonstrates the benefits that can be achieved and provides a basis for further consideration.